This article is the second chapter of a two-part piece looking into five transformative climate finance innovations poised to play a pivotal role in unlocking new sources of funding for green, blue and, more generally, sustainable projects. The first chapter covering Impact Investment funds, Sustainability-Linked Loans and Bonds and Blue Finance can be accessed here.

In this part we explore two types of tools demonstrating a key role in providing structure, consistency, and transparency, in the sustainable finance field: Sustainable Finance Taxonomies and Disclosure Standards. These innovations are gaining global momentum as they are proving instrumental in driving sustainability in the financial sector and facilitating sustainable investments.

Taxonomies for Sustainable Finance

Taxonomies are classification systems that categorise economic activities, assets, or investment projects, based on their alignment with sustainable objectives, such as the SDGs, national goals (i.e. the Nationally Determined Contributions (NDCs)), or the Paris Agreement. Taxonomies establish eligibility criteria, developed by sector specialists and industry experts, to ensure that any particular activity substantially contributes to at least one of its goals (e.g. climate change mitigation, climate change adaptation, biodiversity, circular economy, etc.) while not significantly harming any other. A Green Taxonomy focuses on climate and environmental objectives while a Sustainable Taxonomy includes objectives beyond green and encompasses social objectives.

Such tools bring certainty and transparency to financial markets, encouraging investment in sustainable activities and enabling better tracking of financing flows for sustainability. By offering precise and consistent definitions, Sustainable Taxonomies aim to create reliable, legitimate, unified, and science-based classification systems, reducing the risk of greenwashing and ensuring that sustainability claims are substantiated.

The development trajectory of taxonomies for sustainable financing has focused first on climate change mitigation, with the development of so-called ‘Green Taxonomies’. Since then, additional eligibility criteria have been added progressively to cover all the other aspects of the environmental crisis. For instance, BASE was involved in the development of categorisation systems facilitating investments in local projects contributing to the circular economy in Colombia, Peru, and expanding its work to include Chile, Costa Rica and Uruguay. The transition from a linear to a circular economic system not only contributes towards reducing emissions but also helps address the pressing issue of waste pollution while bringing economic and social positive impacts.

By 2023, more than 35 green and sustainable taxonomy projects have been initiated worldwide, as reported by the United Nations Environment Programme Finance Initiative (UNEP FI). China became in 2015 the first country to adopt a green taxonomy, which currently provides a “white list” of activities and asset types considered “green”. Other influential taxonomies include the Climate Bonds Initiative’s (CBI) Green Bond Taxonomy, the Sustainable Taxonomy of Mexico, and the EU Taxonomy for Sustainable Activities. While these taxonomies can present some differences, they typically share a common foundation.

For example, the CBI Taxonomy, initially published in 2013, offers a general description of sectors and activities, employing a traffic light system to indicate which activities, assets, or projects automatically comply with the taxonomy based on specific criteria. The EU Taxonomy follows a comparable approach, although it uses quantitative metrics and screening criteria. In 2022, Colombia became the first country in the Americas to publish a Green Taxonomy, which includes land management as a notable innovation. Mexico’s Taxonomy, published in 2023, distinguishes itself by considering social objectives alongside environmental objectives, encompassing gender equality and access to basic services related to sustainable cities.

As common denominators, these taxonomies typically share: 1) accelerating the growth of green finance as the primary objective; 2) banks, financial institutions, financial regulators, policymakers and investors as main users; 3) sectoral scopes tailored to the specific needs of the target users; and 4) addressing local environmental objectives in addition to climate change.

To better support the development of such instruments, frameworks building on the common characteristics of already developed taxonomies can be created. To tackle the lack of comparability between national taxonomies in the Latin American region, UNEP FI created the “Common Framework for Sustainable Finance Taxonomies for Latin America and the Caribbean”, that aims to ‘serve as a catalyst for progress towards sustainable finance implementation, providing LAC member states a regional alignment approach to unlock opportunities and financing for long-term value creation, shared prosperity, and sustainable development in the region.’ The Guide to Developing National Green Taxonomy developed by the World Bank serves as another main reference.

Disclosure standards

Taxonomies serve as a shared language, defining terms related to sustainability and providing a common understanding for investors and companies alike. Disclosure standards, on the other hand, build upon this language by specifying the information companies must report. This allows investors to assess the climate-related risks and opportunities associated with a company’s activities. In simpler terms, taxonomies are the building blocks, while disclosure standards are the instructions that ensure investors get a clear picture of a company’s sustainability efforts. Together, these tools play a vital role in promoting transparency and facilitating informed investment decisions.

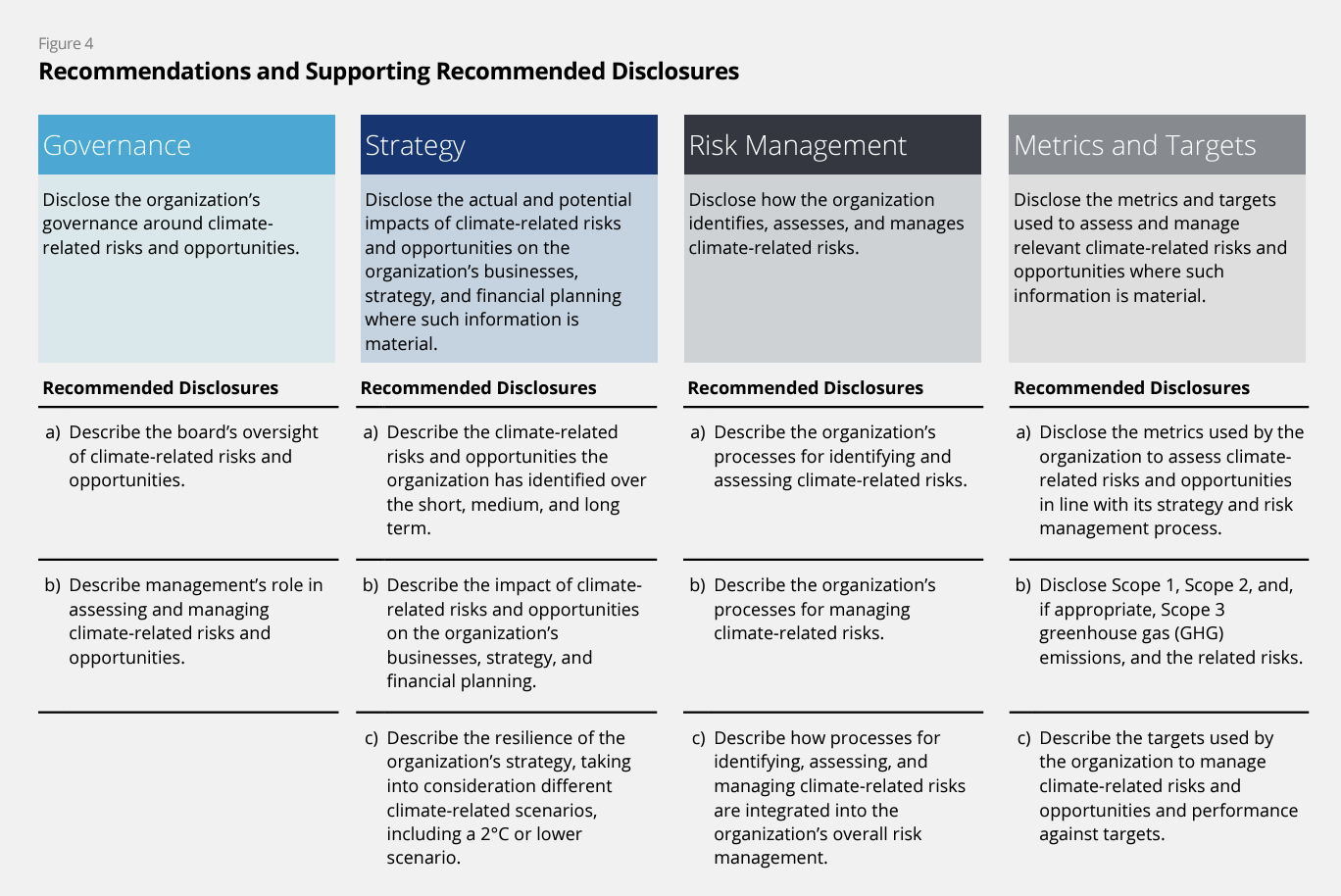

In 2015, the Task Force for Climate-related Financial Disclosures (TCFD), founded by the Basel-based Financial Sustainability Board (FSB), emerged as a game-changer. This voluntary framework provides a set of recommendations for investor-grade risk disclosures on climate change. Designed for use across all industries and jurisdictions, the TCFD promotes consistent and comparable climate-related disclosures by companies. This focus on consistency aimed to push companies to dwell on their climate-related risks and opportunities, and accordingly account for these factors into risk management, strategic planning, and decision-making.

The benefits of disclosures have a ripple effect beyond a company’s internal functioning and reputational value. As both companies and investors gain a deeper understanding of the financial implications of climate change, markets become better equipped to channel investments towards sustainable solutions, resilient business models, and emerging opportunities. The TCFD framework outlines 11 recommended disclosures categorised under four key areas: Governance, Strategy, Risk Management, and Metrics and Targets.

Financial institutions shoulder an additional, crucial responsibility. Beyond disclosing their own climate risks, they must also consider the climate risks associated with the companies they invest in.

In 2020, a consortium of five standard-setting organisations—the Carbon Disclosure Project (CDP), Climate Standards Disclosure Board (CSDB), Global Reporting Initiative (GRI), International Integrated Reporting Council (IIRC), and Sustainable Accounting Standards Board (SASB)—signalled their intention to work towards enhancing corporate reporting to complement financial reporting regarding sustainability. Notably, during these early years, the primary focus of sustainability information was to enhance economic decision-making for enterprise value creation. However, over the past four years, the conversation has rapidly evolved to encompass a broader perspective. Now, it not only considers economic impact but also the environmental and social impacts of an organisation (often referred to as “double materiality”) and its contribution to achieving sustainable development.

These organisations spearheaded efforts to push for robust sustainability reporting alongside financial disclosures. They pursued this goal through both independent research and collaborative initiatives. A key milestone was the merger of SASB and IIRC to form the Value Reporting Foundation (VRF):

- IIRC’s International Integrated Reporting Framework: grounded in principles and applicable across industries, fosters a holistic view of value creation through disclosures on governance, business model, and information interconnectedness.

- SASB standards: Provide 77 industry-specific metrics, enabling crucial comparability of sustainability data among peer companies. In essence, the VRF offers a comprehensive solution, marrying the IIRC’s holistic perspective with the industry-specific comparability facilitated by SASB standards.

Another significant development was the Corporate Reporting Dialogue, which included CDP, CSBD, GRI, ISO, SASB, and IIRC (detailed timeline available here). Ultimately, these efforts culminated in the establishment of the International Sustainability Standards Board (ISSB), now a reference. This comprehensive and globally relevant body aims to provide a standardised baseline for sustainability disclosures within capital markets through its IFRS Sustainability Disclosure Standards.

This standardisation directly addresses the prior issue of fragmented frameworks, often referred to as the “alphabet soup,” which caused confusion regarding adoption and implementation. In essence, the IFRS standards represent a harmonisation of existing frameworks, rather than an erasure of previous work. As a result, companies and capital markets will face reduced complexity and lower costs when applying and using sustainability-linked information.

Before delving into how they facilitate interoperability with other sustainability reporting frameworks, let’s first examine what the IFRS standards entail. This will provide a foundational understanding before we explore how they assist companies in streamlining their sustainability reporting processes and disclosures. As of now, the IFRS sustainability standards consist of two parts: IFRS S1 and IFRS S2.

- IFRS S1: This standard focuses on how companies prepare and report their sustainability information alongside financial statements. It sets clear guidelines for presenting this information to be most helpful for users when deciding to invest in the company.

- IFRS S2: This standard mandates the disclosure of climate-related information with the potential to impact an entity’s financial performance over the short, medium, and long term. This encompasses cash flow, access to financing, and the cost of capital. IFRS S2 emphasises both risks and opportunities associated with climate change, including physical risks (e.g., extreme weather events) and transition risks (e.g., regulatory shifts or evolving consumer preferences). Additionally, IFRS S2 compels entities to report progress towards self-imposed climate targets and adherence to any legally mandated ones.

How, then, does IFRS build upon its predecessors? Notably, IFRS S2 mandates industry-specific disclosures, where it leverages illustrative guidance derived from the SASB Standards. These industry-specific climate-related metrics enhance comparability for investors by aligning with existing industry benchmarks.Furthermore, companies adhering to the IFRS automatically fulfil, and often exceed, the recommendations set forth by the TCFD. One example of how IFRS surpasses TCFD recommendations lies within the “Risk Management” category. While TCFD focuses on a general description of risk identification processes, IFRS S2 delves deeper. It mandates the disclosure of detailed information regarding these processes, including specific data sources, assumptions employed for risk identification, and the role of climate-related scenario analysis. Additionally, companies must report changes made to their risk identification and management processes compared to the previous year. This increased level of granularity provides investors with a clearer picture of a company’s approach to managing climate-related risks. Moreover, companies transitioning from TCFD can seamlessly integrate their existing efforts with IFRS by utilising the IFRS-TCFD interoperability guide.